Different Trusts for Different Purposes

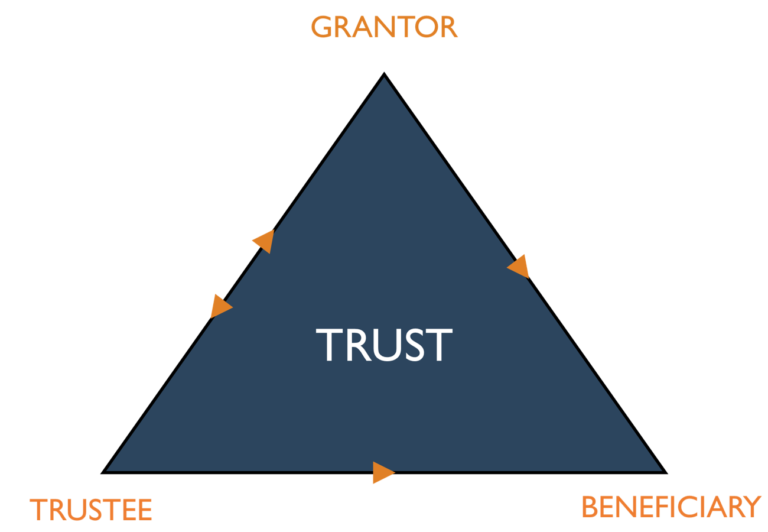

Trusts are legal entities that own assets, and all trusts are not alike. They are created by a written trust document with certain provisions that can vary from trust to trust.

Trusts are legal entities that own assets, and all trusts are not alike. They are created by a written trust document with certain provisions that can vary from trust to trust.

Beneficiaries of a trust typically pay taxes on the distributions they receive from the trust’s income, rather than the trust itself paying the tax. However, these beneficiaries are not subject to taxes on distributions from the trust’s principal.

Certain types of trusts, however, may only be used in very specific situations and a constructive trust is one of them.

A trust is often only as good the trustee in charge of it. Read on, as we examine the important role of the trustee and discover how to make sure yours is acting correctly, especially with complex instruments like insurance.

A trust can be used to manage estate taxes, shelter assets from creditors and pass on wealth to future generations. A family trust is a specific type of trust that families can use to create a financial legacy for years to come. There are several benefits to creating one, although not every family necessarily needs one. If you’re curious about where this type of trust might fit into your family’s estate plan, here’s what you need to know.

One of the most fundamental choices you can make as you’re thinking about how to pass your assets on to heirs, is whether you hold assets in a revocable trust or more simply give them via a will. Both approaches have advantages, although trusts can provide significantly more benefits.

When is the last time you updated your will? Could your beneficiaries have changed? If you have a trust, did you actually fund it? Is your plan ready for the new SECURE Act? Here are five mistakes you don’t want to make.

If you’ve heard of trust funds but don’t know what they are or how they work, you’re not alone. Many people know just one key fact about trust funds: they’re set up by the ultra-wealthy as a way to protect passing on significant sums of money to family, friends or entities (charities, for example) after they pass away.

Do you ever worry about how your beneficiaries will manage their portion of their inheritance when you pass away? One solution that allows you to still exert some control over your money–even after passing–is with a revocable living trust (RLT).

Failing to ensure that your asset titling and beneficiary designations are coordinated with your estate plan, can lead to unintended costs, taxes and outcomes.